What is Cointegration? How to understand the concept of Cointegration in simple terms without the help of technical jargon. what is the difference between cointegration and correlation?

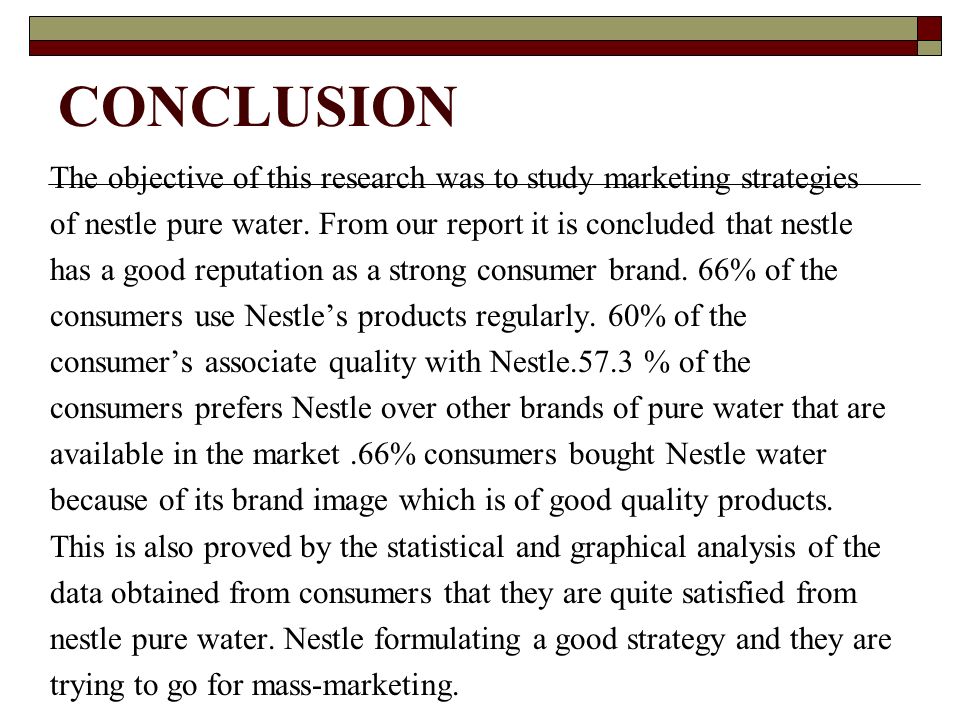

This chapter deals with the presentation, analysis and interpretation of results based on the objectives. The estimation results of the model are supported and further analyzed by using the relevant econometric techniques viz. Descriptive statistics, coefficient of determination, standard error, t- statistics etc.

ECMs are a theoretically-driven approach useful for estimating both short-term and long-term effects of one time series on another. The term error-correction relates to the fact that last-period's deviation from a long-run equilibrium, the error, influences its short-run dynamics. Thus ECMs directly estimate the speed at which a dependent.

This example Error Correction Model Essay is published for educational and informational purposes only. If you need a custom essay or research paper on .READ MORE HERE.